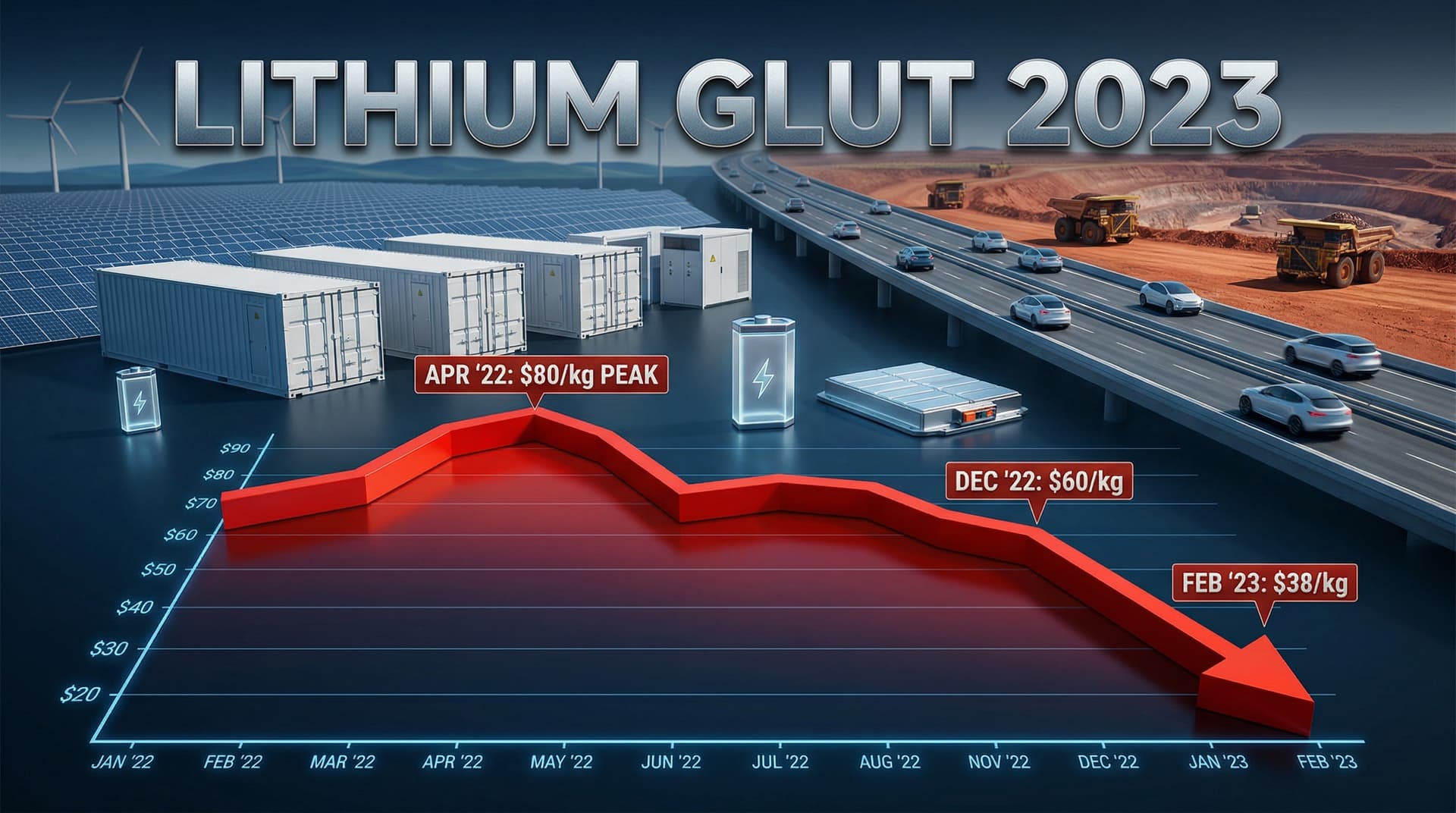

In a dramatic turn for the battery metals market, spot prices for lithium carbonate have plummeted to their lowest levels in over two years. As of early February 2023, battery-grade lithium carbonate prices in China have fallen below 265,000 CNY per tonne ($38/kg), down more than 12% in the past week alone and over 50% from peaks last April. This collapse, tracked by Fastmarkets and other benchmarks, signals the end of the lithium boom that fueled massive investments in mining and battery production.

The decline caps a sharp downward trajectory that began in late 2022, when prices hovered above $70/kg amid supply shortages. Now, with inventories building and demand growth slowing, the market is awash in the key ingredient for lithium-ion batteries powering electric vehicles (EVs), consumer electronics, and rapidly expanding grid-scale energy storage systems.

Anatomy of the Price Collapse

Lithium carbonate, the most traded lithium product for batteries, has seen relentless pressure. Spot prices for 5.5% lithium carbonate equivalent (LCE) battery-grade material traded at 260,000-270,000 CNY/t in China this week, equivalent to roughly $37-39/kg. This marks the lowest since February 2021, before the explosive demand surge from the EV boom.

Hydroxide prices, used in high-nickel cathodes, have followed suit, dipping below $45/kg. In contrast to 2022's spot frenzy, contract prices are renegotiating lower, with Asian EV battery makers securing deals 20-30% below last quarter's levels.

Global lithium supply has ballooned. Australia, the top producer, ramped up output from giants like Greenbushes and Pilgangoora, hitting record exports in Q4 2022. New projects in Argentina's 'Lithium Triangle'—from Livent, Allkem, and POSCO—began flowing spodumene concentrate to China for conversion. Chinese converters, idled during 2022 COVID lockdowns, restarted aggressively post-reopening, exacerbating the glut.

| Metric | Peak (Apr 2022) | End-2022 | Feb 4, 2023 |

|---|---|---|---|

| Li2CO3 Spot (USD/kg) | 82 | 45 | 38 |

| Supply Growth YoY | - | +140% | +175% projected |

| China EV Sales YoY (Jan) | - | +30% | +2.4% |

(Data compiled from Fastmarkets, Benchmark Minerals, CAAM)

Demand Softens Amid Economic Headwinds

Demand drivers are faltering. China's passenger EV sales rose just 2.4% year-on-year in January 2023, hampered by a faltering post-COVID recovery and subsidy phase-outs. While Tesla and BYD posted gains, overall new energy vehicle (NEV) penetration hit 33% but growth slowed sharply from 2022's 90% surge.

Europe faces headwinds too: EV registrations fell 10% in December 2022 amid subsidy cuts in Germany and high energy costs. The US saw robust growth but remains a fraction of China's volume. Energy storage, a bright spot, accounted for ~10% of battery demand in 2022 per IEA estimates, but grid projects are still ramping.

Boon for Energy Storage Deployment

Cheaper lithium is music to the ears of energy storage developers. Lithium-ion battery pack prices, already down 14% in 2022 to $139/kWh per BloombergNEF's Q4 survey, could accelerate toward the $100/kWh threshold this year. This directly slashes levelized cost of storage (LCOS) for grid applications.

In the US, the Inflation Reduction Act (IRA) of 2022 supercharges this trend. Production tax credits under Section 45X offer up to $35/kWh for domestic battery cells, $10/kWh for modules, and bonuses for using North American-sourced minerals—up to 10% of cell value. Projects like NextEra's 409 MW/1,638 MWh Manatee Energy Storage Center in Florida, approved late 2022, exemplify the boom, with commissioning slated for 2024.

Australia, home to 52% of global lithium, sees storage tenders filling up: tender for 2.4 GW/5 GWh in New South Wales closed in January. Europe’s grids, strained by gas shortages, awarded 5 GW+ in recent auctions, with prices dipping below €40/MWh discharge.

Lower input costs enable fiercer bidding. Fluence Energy, a leader in grid storage, noted in its Q3 earnings that supply chain stabilization is aiding margins. Developers like Plus Power and Primergy are stacking projects, targeting 10 GW deployment in 2023.

Policy and Market Responses

Policymakers are recalibrating. The IRA's 'foreign entity of concern' (FEOC) rules—proposed by Treasury in December 2022—bar tax credits for batteries with >25% components from China, Russia, etc., by 2024. This spurs US refining: Albemarle's $1.3 billion expansion in North Carolina and Silver Peak, Nevada; Livent's Argentina-US corridor.

Australia's Critical Minerals Strategy invests A$15 billion in downstream processing, aiming to capture more value. The EU's proposed Batteries Regulation, advancing through 2023, mandates 16% recycled content by 2030 and a battery passport for traceability.

Miners are hurting: Pilbara Minerals slashed guidance, idling Kwinana plant. Core Lithium mothballed Finniss. SQM and Albemarle face Q4 2022 results scrutiny next week, with writedowns likely. Yet giants like Ganfeng and Tianqi hold firm, betting on long-term tightness.

Battery majors benefit: CATL, BYD vertically integrate, locking in upstream. LG Energy Solution and Panasonic report cost relief in EV packs.

Outlook: Glut Today, Scarcity Tomorrow?

Analysts project a 2023 surplus of 100,000-200,000 tonnes LCE, but demand could rebound with EV sales normalizing to 30%+ growth. IEA forecasts battery demand doubling to 1.3 TWh by 2025, with storage claiming 20% share. S&P Global sees deficit by 2026 as mines lag 5-7 year timelines.

For energy storage news watchers, this dip is a market reset: accelerating near-term builds while policies harden supply chains against volatility. Grid operators from California ISO to National Grid UK stand to gain as BESS economics improve amid renewables integration crunch.

The lithium rollercoaster underscores energy transition risks—commodity swings threaten IRA goals unless domestic capacity scales fast. As prices stabilize, expect consolidation: stronger miners acquire juniors, battery firms double down on LFP chemistries less reliant on pricier nickel.

(Word count: 912)