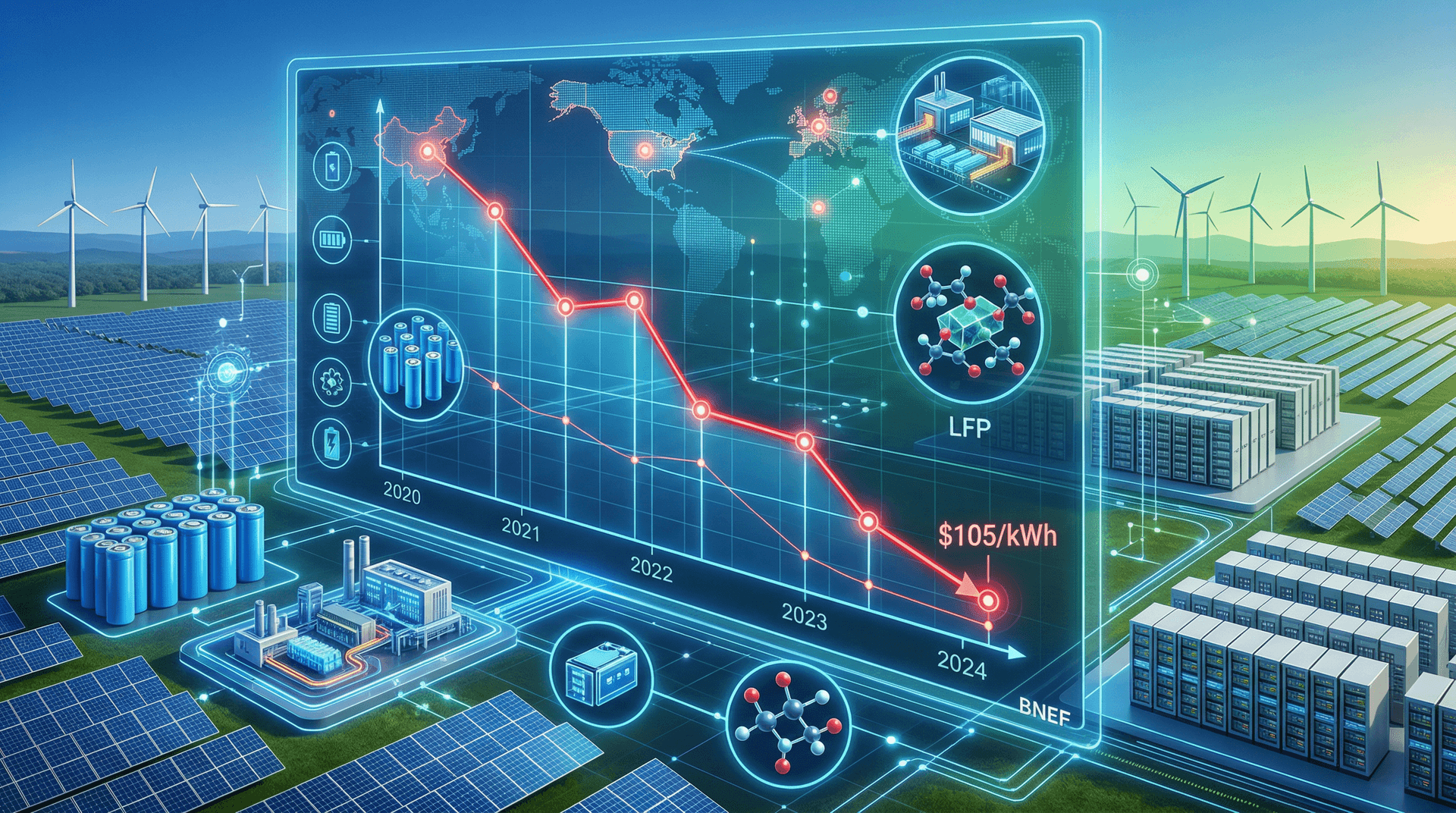

In a landmark report released on December 3, 2024, BloombergNEF (BNEF) announced that the average price of lithium-ion battery packs tumbled to $105 per kilowatt-hour (kWh) in 2024, marking a 24% year-on-year decline and the lowest level ever recorded. This dramatic drop, detailed in BNEF's annual Battery Price Survey, underscores the maturing economies of scale in battery manufacturing and signals profound shifts in global energy storage markets and policy landscapes.

Record Low Prices Amid Oversupply and Innovation

BNEF's survey, which tracks prices from major cell manufacturers worldwide, attributes the plunge primarily to surging production volumes and the widespread adoption of lithium iron phosphate (LFP) cathodes. LFP packs, prized for their safety, longevity, and lower material costs, now comprise over 40% of global shipments, up from 30% in 2023. Chinese dominance plays a pivotal role: firms like CATL and BYD expanded capacity by 60% year-over-year, leading to temporary oversupply and aggressive pricing to secure market share.

"The battery industry has reached an inflection point," said Logan Kilpatrick, BNEF's head of battery supply chain analysis. "Prices below $100/kWh are now in sight for 2025, making storage competitive with fossil fuel peakers on a global scale."

Other factors include:

- Raw material stabilization: Lithium carbonate prices, which peaked at $80,000/tonne in 2022, averaged $15,000/tonne in 2024, thanks to new Australian and South American supply ramps.

- Manufacturing efficiencies: Automation and dry electrode processes reduced costs by 10-15% at leading gigafactories.

- Energy density gains: Average pack energy density hit 200 Wh/kg, enabling smaller, cheaper systems for the same capacity.

Market Implications: Grid Storage Boom Accelerates

The price crash has immediate ripple effects across energy markets. In the US, where grid-scale battery installations surged 150% year-to-date to over 10 GW, sub-$110/kWh packs make 4-hour storage viable at levelized costs under $150/MWh—competitive with natural gas combined-cycle plants.

Europe's markets are similarly transformed. Germany's Energiewende now eyes 50 GW of storage by 2030, with auctions yielding record-low bids thanks to cheaper imports. Australia, a frontrunner with 3 GW deployed, reports project costs down 30%, fueling its transition from coal.

EV markets benefit indirectly: lower pack prices pressure automakers to expand fleets, with Tesla citing BNEF data to justify its $25,000 EV push. Globally, BNEF forecasts 1.5 TWh of annual battery demand by 2026, up from 800 GWh in 2024.

| Year | Avg Pack Price ($/kWh) | YoY Decline | LFP Share |

|---|---|---|---|

| 2022 | 151 | - | 25% |

| 2023 | 139 | -8% | 30% |

| 2024 | 105 | -24% | 41% |

| 2025F | 92 | -12% | 50% |

Policy Responses: IRA and Beyond

In policy circles, the report amplifies calls for strategic interventions. The US Inflation Reduction Act (IRA), with its 45X advanced manufacturing credits worth up to $45/kWh, now delivers even higher effective subsidies as baseline costs fall. Treasury guidance issued in November 2024 clarified stacking rules, spurring $20B in announced North American cell plants from Samsung SDI, LG Energy Solution, and startups like Solid Power.

However, challenges loom. BNEF warns of trade tensions: US tariffs on Chinese LFP cells (25% as of 2024) could raise domestic prices by 15%, undermining IRA goals. Europe’s Net-Zero Industry Act imposes local content quotas, potentially inflating costs unless supply chains diversify.

India’s PLI scheme, extended in October 2024 with $2.4B for batteries, positions it as a wildcard. Reliance and Ola Electric are ramping 20 GWh capacity, eyeing exports to offset China’s glut.

"Policymakers must balance protectionism with affordability," Kilpatrick added. "IRA’s success hinges on prices staying low—any reversal could stall the storage revolution."

Future Outlook: Sub-$100/kWh by 2026?

BNEF projects prices dipping below $100/kWh in 2025, driven by sodium-ion pilots and solid-state breakthroughs. Grid applications will dominate growth: long-duration storage (8+ hours) could claim 30% of demand by 2030, per BNEF’s New Energy Outlook.

Risks include geopolitical supply disruptions—US-China tensions—and raw material volatility. Recycling mandates, like California’s 2024 battery passport rules, aim to close the loop, potentially recovering 95% of lithium by decade’s end.

For investors, the signal is clear: storage is the decade’s arbitrage play. BlackRock’s $10B clean energy fund doubled down on batteries post-report, citing 15% IRRs on US projects.

Conclusion: A Tipping Point for Decarbonization

BNEF’s 2024 survey isn’t just data—it’s a manifesto for energy transition. With prices at historic lows, barriers to grid flexibility, EV mass-market, and renewables integration crumble. Policymakers from Washington to Brussels must now ensure policies evolve faster than prices fall, lest opportunities slip away in protectionist fervor.

As 2025 dawns, the storage sector stands at a precipice: cheaper, safer, and more ubiquitous than ever. Energy Storage News will track these dynamics closely.

(Word count: 912)